This article is to give us an idea of what is LEI, the circumstances which were contributors to the emergence of this concept LEI, the background of how it all starts, formulated, devised and currently monitored, the impact that it has created since its implementation.

BACKGROUND

Following the collapse of Lehman Brothers in 2008, which led to a global financial crisis, an urgent need was felt to take control over the Financial Markets Transactions that was lacking globally. The inability to identify through one unique identity, the exposure of Corporates which were operating globally left Financial Regulators with no clue, and huge time and cost involvement to identify the collapse and also the impact of the same.

HOW WAS THE IDEA OF A SINGLE UNIQUE IDENTIFIER CONCEIVED?

The concept is not new and dates back to 40 years, when Wrigley’s Chewing Gum started a business revolution by introducing barcode system in its chewing gum pack that can be scanned under an electronic reader. This was the first time anything had “read” an item with a standardized 11digit barcode label.

Once Lehman Brothers collapsed, the need for bringing about a similar revolution in the Financial Markets sector was felt and hence LEI was born.

Regulators all over the globe started introducing new norms and regulations to be followed which led to complex data ecosystems, and companies found it very difficult to comply with different regulations in different geographies. LEI was a common thread that ran through Regulations in most of the jurisdictions.

The main objective of this LEI was to trace all layers of an Entity globally, along with their relationship with each of those associated entities with one Unique Identification number which will make risk assessment easier, cost effective and also make data availability to investors worldwide a very transparent process.

FINANCIAL STABILITY BOARD:

In 2009, the G20 forum endorsed the Financial Stability Board Charter. (FSB) is an international body that monitors and makes recommendations about the global financial system. It does so by coordinating national financial authorities and international standard-setting bodies as they work towards developing strong regulatory, supervisory and other financial sector policies. The FSB, working through its members, seeks to strengthen financial systems and increase the stability of international financial markets.

GLOBAL LEI:

In 2011, the G20 called on the FSB to take the lead in developing recommendations for a global LEI and a supporting governance structure.The FSB is the founder of the Global Legal Entity Identifier Foundation (GLEIF) and appointed the first GLEIF Board of Directors and was founded in 2014. The Global Legal Entity Identifier Foundation (GLEIF) is tasked to support the implementation and use of the LEI. GLEIF is a supra-national not-for-profit organization headquartered in Basel, Switzerland.

GLEIF manages a network of partners, known as the LEI Issuing Organizations to provide trusted services and open, reliable data for unique legal entity identification worldwide.

Following the financial crisis, the goal of the drivers of LEI Initiative - the Group of 20, the Financial Stability Board and many regulators around the world – was to use the LEI to create transparency in the derivatives markets.The Vision of LEI is to create one Global Identity Behind every Business.

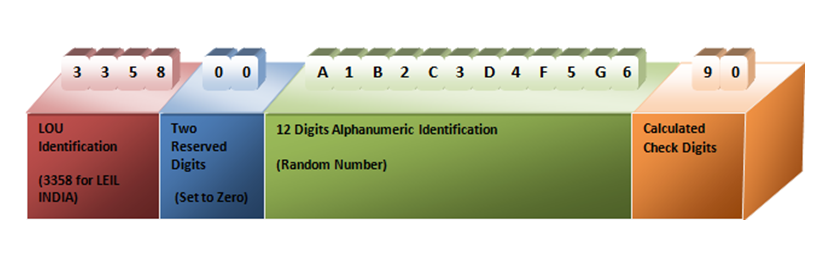

WHAT IS LEI?

LEI is a 20-digit identification number, that is used for consistent and accurate identification of all legal entities that are parties to financial transactions. It also enables a legal party to a financial transaction to be identified precisely.

LEI STRUCTURE:

LEI IMPLEMENTATION IN INDIA:

The GLEIF has appointed various LOUs (Local Operating Units) giving them the authority to issue LEIs as per the policies and regulations issued by FSB. CCIL (Clearing Corporation of India Limited) is designated as the LOU in India.

Legal Entity Identifier India Limited, a wholly owned subsidiary of CCIL acts as a LOU for issuing Global Legal Entity Identifiers in India. LEIL has been recognized by the Reserve Bank of India as an “Issuer” of Legal Entity Identifiers under the Payment and Settlement Systems Act 2007 (as amended in 2015).” LEIL has been Accredited by the Global Legal Entity Identifier Foundation (GLEIF) as a Local Operation Unit (LOU) for issuance and management of LEI's.

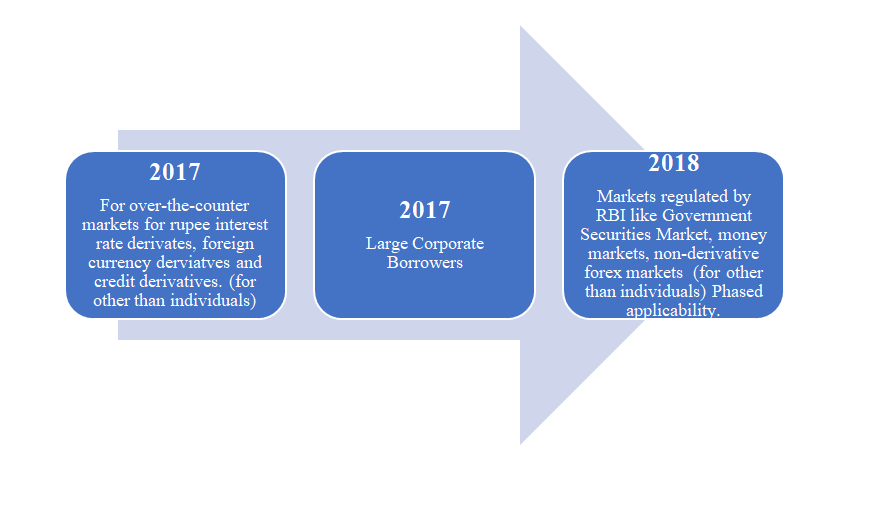

PHASED IMPLEMENTATION IN INDIA:

Ref Circulars of RBI dated 29th November 2018 and 2nd November 2017.

Now let’s see the timelines specified by RBI for Large Corporate Borrowers and Non-Derivative Market Participants to obtain LEI in India:

LARGE CORPORATE BORROWERS:

| Phase | Timeline |

|---|---|

| Phase I- Total Exposure to SCB’s of Rs 1000 crore and above | 31st March 2018 |

| Phase II- Total Exposure to SCB’s between Rs 500 crore and 1000 crore | 30th June 2018 |

| Phase III- Total Exposure to SCB’s between Rs 100 crore and 500 crores | 31st March 2019 |

| Phase IV- Total Exposure to SCB’s between Rs 50 crore and100 crores | 31st December 2019 |

NON-DERIVATIVE MARKET PARTICIPANTS:

| Phase | Timeline |

|---|---|

| Phase 1- Net Worth of Entities above Rs 10,000 million | April 30th 2019 extended to 31st December 2019 |

| Phase 2- Net Worth of Entities between Rs 2000 million and Rs 10,000 million | August 31st 2019 extended to 31st December 2019 |

| Phase 3 - Net Worth of Entities up to Rs 2000 million | 31st March 2020 |

Note

In case of non-derivative forex transactions, client transactions shall require LEI code for transactions involving an amount equivalent to or exceeding USD one million or equivalent thereof in other currencies.

PROCESS TO APPLY LEI:

- Step 1 Applicant should apply for it online Apply https://www.ccilindia.lei.co.in

- Step 2 Applicant authorized by the Board should create an online account.

- Step 3Applicant should prepare and submit the online application along with the necessary fee payment.

- Step 4 The Applicant should submit the necessary documents along with the registration form.

- Step 5 LEIL will verify the documents submitted, payment and online form.

- Step 6 LEI number is issued generally within 3 to 5 working days.

CONCLUSION

The Introduction of LEI is to bring benefits to both financial market regulators as well as market participants. As per the Statistics of Global Legal Entity Identifier Foundation, so far 15,45,783 LEIs have been issued. It has also been reaping the benefits it is intended to so far. It is also seen that based on an Assessment performed on 31st December 2019, it shows that the absolute number of data quality failures reduced by 23K compared to the end of 2018. The overall maturity level of the data improved in 2019 and the percentage of LEI issuers at the required quality level remains stable above 90% also for the reporting period.

Companies Act 2013

IAL AUDIT CA Santhipriya S

APPOINTMENT OF COMPANY SECRETARY:

As per Section 203 of the Companies Act, 2013, every company belonging to certain class or classes of companies as may be prescribed shall mandatorily appoint certain Key Managerial personnel (KMP) in their company on a whole-time basis and Company secretary is one such KMP role which the prescribed companies have to mandatorily appoint in their Company. In the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 the classes of companies are prescribed through rule 8 that every listed and every other public company having paid-up share capital of Rs.10 crores or more shall appoint whole-time Key managerial personnel. On 9th of June, 2014 Rule 8A was introduced to mandate every Private company which has a paid up share capital of Rs. 5 crores or more to appoint a whole time Company Secretary.

Though Private Companies having paid up capital of Rs. 5 Crores or more were mandatorily required to employ a whole time Company secretary since June 2014, many companies were non-compliant of this provision since a Private Company normally would not have much of requirements for a Company secretary to perform in their Company except for maintaining minutes of meetings and filing annual returns with ROC which the Company can prepare and maintain it internally with the help of practicing Company secretary at a cost much lower than what has to be paid to a Company secretary if appointed. Many Private companies even after the Rule 8A came into place did not appoint a Company secretary whole time due to costs and only few functions that a Company Secretary can offer to a Private Limited Company Compared to that of a Public or Listed Company.

In 2019, MCA introduced form INC-22A called as ACTIVE form to ensure the KYC details of the Company and the consequences of non-filing of the ACTIVE form was severe that the Companies have to mandatorily comply with this one time ACTIVE form failing which the Company cannot file forms with ROC relating to any changes like authorized capital change, directors change, etc., And the design of the form was such that if there were any non-compliance by the Company relating to Company secretary appointment or Auditors appointment, without complying with the provisions relating to that, the Company cannot file ACTIVE form. Hence, all Private Companies which were non compliant of Section 203 were forced to appoint a Company secretary primarily to file the ACTIVE form.

Since the introduction of ACTIVE forms, the demand for a Company secretary has increased and in certain cases, the Companies were forced to pay the amounts demanded by Company Secretaries even in Companies where they do not have many roles to play and illegitimate practice of name lending by Company Secretaries were prevalent during this period. In this scenario, on 3rd Jan 2020, Rule 8A is amended to increase the threshold limit for appointment of Company secretaries by Private Companies and hence Private Companies which has a paid up capital of Rs.10 Crores or more has to mandatorily appoint a whole time Company Secretary.

Thus, only Listed Companies, Unlisted Public Companies and Private Companies which has a paid up Capital of Rs.10 Crores or more has to mandatorily appoint a whole time Company Secretary. Due to this amendment, the demand for Company secretaries looking for employment would drastically reduce and the Company Secretaries who were appointed by Companies having paid up Capital of more than Rs.5 Crores and not more than 10 Crores would lose their job as it is no more mandatory for the Company to appoint a whole time CS.

SECRETARIAL AUDIT:

As per Section 204 of the Companies Act, 2013 every listed Company and other Companies belonging to certain class or classes of Companies as may be prescribed shall annex it’s Board report with a Secretarial audit report prepared by a practicing Company Secreatary. Rule 9 of the Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014 prescribes the following class of Companies for which Secretarial audit would apply:

- Every public Company having paid up Capital of Rs.50 Crores or more

- Every Public Company having turnover of Rs.250 Crores or more

- With effect from 3rd Jan 2020, every Company (whether public or private) having outstanding or borrowings from banks or financial institutions of Rs.100 Crores or more.

Thus, the amendments brought in through the Companies (Appointment and Remuneration of Managerial Personnel) Amendment Rules, 2020 dated 3rd January 2020 has removed the burden of Private Companies having paid up capital less than 10 crores from having a full time Company secretary and increased the Compliance requirements of all categories of Companies having more than Rs.100 Crores of borrowings from Banks or financial institution by mandating Secretarial audit to such companies.

TAXATION

CA Srinidhi S

E-Invoicing under GST

GST e-invoice is the introduction of the digital invoice for goods and services provided by the business firm generated at the government GST portal. The concept of GST e-invoice generation system has been taken into consideration for the reduction in GST evasion.

‘E-invoicing’ or ‘electronic invoicing’ is a system in which B2B invoices are authenticated electronically by GSTN for further use on the common GST portal.Under the proposed electronic invoicing system, an identification number will be issued against every invoice by the Invoice Registration Portal (IRP) to be managed by the GST Network (GSTN).All invoice information will be transferred from this portal to both the GST portal and e-way bill portal in real-time.Therefore, it will eliminate the need for manual data entry while filing ANX-1/GST returns as well as generation of part-A of the e-way bills, as the information is passed directly by the IRP to GST portal.

Applicability

The GST Council has approved introduction of ‘E-invoicing’ or ‘electronic invoicing’ in a phased manner for reporting of business to business (B2B) invoices to GST System, starting from 1st January 2020 on voluntary basis.

- Turnover 500 Crore or More – Voluntary and Trial Basis start from 1st January 2020

- Turnover 100 Crore or More – Voluntary and Trial Basis start from 1st February 2020

It is proposed that the E-Invoicing shall be made mandatory with effect from 1st April 2020 for the above business.

Since there was no standard for e-invoice existing in the country, standard for the same has been finalized after consultation with trade/industry bodies as well as ICAI after keeping the draft in public place. Having a standard is a must to ensure complete inter-operability of e-invoices across the entire GST eco-system so that e-invoices generated by one software can be read by any other software, thereby eliminating the need of fresh data entry – which is a norm and standard expectation today. The machine readability and uniform interpretation is the key objective. This is also important for reporting the details to GST System as part of Return. Apart from the GST System, adoption of a standard will also ensure that an e-invoice shared by a seller with his buyer or bank or agent or any other player in the whole business eco-system can be read by machines and obviate and hence eliminate data entry errors.

Process for generating E-Invoicing

GSTN and ICAI collaborated to design the standard format of e-invoice for businesses operating in India.This refers to PEPPOL (Pan European Public Procurement Online), which is based on the UBL (Universal Business Language) standard. Any existing accounting or invoicing software/ application provider (SAP/Tally/Busy) must follow the PEPPOL standard for invoice generation. Taxpayers will, therefore, be able to generate a compliant invoice at the source. Currently, PEPPOL is the most used standard across the globe. The system advocates diversified business applications and trading communities to exchange information along their supply chains using a common or a standard format. It enables a single point of data entry into electronic commerce for businesses. Thereafter, the data flows across different portals with the help of an IRP.

The software focuses on the prevailing tax laws and even incorporate features supporting international trade. The information required by the government on a primary basis is marked as mandatory in the e-invoice others are marked as optional fields in the form.

Generation of invoice in standard format

Generation of e- invoice will be the responsibility of the tax payer in his own accounting / billing system. It can be any software utility that generates invoices ie SAP/ TALLY or Excel based utility. The most important point here is that the invoice must have mandatory parameters and must conform to the e-invoice standard( schema) published in GST common portal https://www.gstn.org/e-invoice/"

The optional parameters can be according to the business need of the supplier.The supplier’s software should be capable to generate a JSON of the invoice that is ready to be uploaded to Invoice reference portal( IRP) of GST.

Reporting of e- invoice to a central system

Invoice Registration portal( IRP) of GST will check from Central Registry of GST system to ensure that same invoice from same supplier pertaining to same financial year is not being uploaded again.

On receipt of confirmation, it will generate a unique Invoice Reference Number( IRN) and digitally sign the invoice and also generate a QR Code. Portal will return the same to the taxpayer who generated the document. The IRP will also send the signed e invoice to the recipient of the document.

E invoice data would be used by GST system for generation of e way bill( Part 1) and updating ANX-1 of the seller and ANX-2 of the buyer.The QR code will contain viral parameters of the invoice ie GSTN of seller, buyer invoice no., invoice date, number of line items, HSN of major commodities.

The e-invoice will be digitally signed by the IRP after it has been validated. Once it is registered, it will not be required to be signed by anyone else.The Logo will not be sent to IRP. It will not be part of JSON file to be uploaded on the IRP. However, software company can provide LOGO in the billing/accounting software so that it can be printed on invoice using the printer.

Benefits of Implementing E-Invoicing System

- E-invoice resolves and plugs a major gap in data reconciliation under GST to reduce mismatch errors.

- E-invoices created on one software can be read by another, allowing interoperability and help reduce data entry errors.

- Real-time tracking of invoices prepared by the supplier is enabled by e-invoice.

- Backward integration and automation of the tax return filing process – the relevant details of the invoices would be auto-populated in the various returns, especially for generating the part-A of e-way bills.

- Faster availability of genuine input tax credit.

- Lesser possibility of audits/surveys by the tax authorities since the information they require is available at a transaction level.

Trending Topics

CA Rohith Rav

IND AS 40 – INVESTMENT PROPERTY

The primary purpose of Ind AS 40 is to introduce and establish targeted accounting for strategic investments made by entities in properties to earn some kind of rentals or value appreciations in future.The separate standard for Investment Properties indicates the sufficiently different characteristics of investment properties as against the owner-occupied properties.

Thereby, the perspective of recognizing and accounting for properties expand broadly into 3 categories

- Ind AS 16 :

Property, Plant & Equipment. - Ind AS 17 :

Leases. - Ind AS 40 :

Investment Property.

The following aspects shall be covered in this article

- What is Investment Property?

- Concept of Owner-occupied Property

- Criteria for Initial Recognition

- Subsequent Measurement of Investment Property

- Disclosure requirements

WHAT IS INVESTMENT PROPERTY?

Investment property is property (land or a buildingor part of a buildingor both) held, by the owner or by the lessee under a finance lease,for the following specific purposes –

- To earn rentals

- For capital appreciation

- Both

Investment property are not utilized for the following

- Use in the production or supply of goods or services or for administrative purposes

- Sale in the ordinary course of business.

Example -Property intended for sale in the near term; Property being constructed for a third party

Examples of Investment Properties

- Land or Building held for long term capital appreciation.

- Land or Building owned by the entity under Finance Lease.

- Vacant Building let out under operating lease.

- Property being constructed for future use as investment property.

CONCEPT OF OWNER-OCCUPIED PROPERTY

Owner-occupied property is property held by the owner or by the lessee under a finance leasefor use in the production or supply of goods or services or for administrative purposes.

Investment property generates cash flows largely independently of the other assets held by an entity. The generation of independent cash flows through rental or capital appreciation distinguishes investment property from owner-occupied property.

Judgement is needed to determine whether a property qualifies as investment property.

Dual Purpose Properties:

Some properties comprise a portion that is held to earn rentals or for capital appreciation and another portion that is held for use in the production or supply of goods or services or for administrative purposes.

- If both portions are separable, i.e. (could be sold or leased out separately under finance lease), then entity should account for each portion on individual basis.

- If both portions are not separable, i.e. (could not be sold or leased out separately under finance lease), the propertywill be treated as Investment Property only, if an immaterial part of such property is held for use in theproduction, supply of goods/services or for use in administration.

Example – Sun Ltd owns a building having 15 floors of which it uses 5 floors for its office; the remaining 10 floors are leased out to tenants under operating leases. According to law company could sell legal title to the 10 floors while retaining legal title to the other 5 floors. In the given scenario, the remaining 10 floors should be classified as investment property, since they are able to split the title between the floors.

Ancillary Services

Investment property should not include Ancillary Services (Meals, Cleaning, Security, Utilities, and Maintenance services). If in case of a certain property, an entity provides ancillary services to the occupants of a property, the entity shall apply the following

- The property will be Investment Property, if quantum of the services is immaterial or insignificant.

- The property will not be Investment Property, if quantum of the services is material or significant.

Example – The owner of an office building provides security and maintenance services to the lessees who occupy the building.

In other cases, the services provided are significant.

Example – If an entity owns and manages a hotel, services provided to guests are significant to the arrangement as a whole. Therefore, an owner-managed hotel is owner-occupied property, rather than investment property.

INITIAL RECOGNITION

A property will be recognized as Investment Property if it meets the following criteria

- The definition of Investment Property

- If future economic benefits are probable to flow to the entity

- Its cost is reliably measurable.

Initial Measurement

The Investment Property is initially measured at Cost including all directly attributablecosts.The cost of Investment Property includes

- Purchase price

- Any directly related cost such as (professional or legal charges, property transfer taxes & any other transaction costs).

The method prescribed under Ind AS 16 – Property, Plant and Equipment shall be adopted for computing the initial cost of Investment Property.

However, if any asset acquired under Finance Lease is classified as Investment Property, the initial recognition principle shall be as per Ind AS 17 – Leases, i.e. the asset shall be recognised at the lower of the fair value of the property and the present value of the minimum lease payments.

Replacement and Derecognition

Parts of investment properties may have been acquired through replacement. Under the recognition principle, an entity recognises in the carrying amount of an investment property the cost of replacing part of an existing investment property at the time when such cost is incurred. The carrying amount of those parts that are replaced is derecognised in accordance with the derecognition provisions.

SUBSEQUENT MEASUREMENT

IAS 40 allows entities an option to apply either the cost model or fair value model for subsequent measurement of its investment property.

However, Ind AS 40 does not permit the use of fair value model for subsequent measurement of investment property.

Under Cost model entity will measure the investment Property as per Cost Model rules prescribed in Ind AS 16, i.e. Cost less Accumulated Depreciation less Accumulated impairment loss.

Fair Value Disclosure

Entities are required to measure the fair value of investment property, for the purpose of disclosure even though they are required to follow the cost model. An entity is encouraged, but not required, to measure the fair value of investment property on the basis of a valuation.

The primary reason for not recognizing fair value of investment property in India is because the derived fair values are not reliable and also using fair value model may lead to recognition and distribution of unrealized gains. However, India is introducing new reforms to provide a boost to the infrastructure and real estate sector, thus facilitating the entities to adopt fair value model for investment properties.

DISCLOSURES

The following disclosures shall apply in addition to disclosures prescribed under Ind AS 17Leases

- Accounting policy for measurement of investment property

- The criteria to distinguish investment property from owner-occupied property and from property held for sale.

- The extent to which the fair value of investment property is based on a valuation by a qualified independent valuer.

- If there has been no such fair valuation, that fact must be disclosed along with the explanation as to why it cannot be measured reliably.

- The amounts recognised in profit or loss for –

- Rental income from investment property.

- Direct operating expenses arising from investment property.

- Depreciation rates, useful lives, gross carrying amount and accumulated depreciation.

- Reconciliation of carrying amount of investment property at the beginning and end of the period.