Interim Budget 2019 Highlights

-CA Srinidhi S

For Farmers:

- New Scheme- namely “Pradhan Mantri KIsan SAmman Nidhi (PM-KISAN)” to extend direct income support at the rate of Rs. 6,000 per year to farmer families, having cultivable land up to 2 hectares is announced.

- Farmers having up to 2 hectares of lands will get Rs 6,000 per year in three equal instalments. The scheme will be effective from December 1, 2018.

- Interest subvention for farm loan takers:

- Farmers affected by natural calamities to get 2% interest subvention and additional 3% interest subvention upon timely repayment.

- 2% interest subvention to farmers who pursue animal husbandry, fisheries jobs through Kisaan credit cards

- Kamdhenu scheme for animal husbandry.

Income Tax reliefs:

Personal Income Tax

- There are no changes in personal income tax rates and slabs.

- Rebate under section 87A is proposed to be increased to INR 12500 from INR 2500 on tax for total income up to INR 5 lakhs for individuals

Instead of giving straight exemption on income up to INR 5,00,000/- finance minister twisted the situation by giving Rebate under section 87A. Thus, if income is more than 5 lakhs, assessee cannot claim rebate under section 87A and assessee will need to pay tax on income above INR 2,50,000/- Explained with below example:

| Particulars |

Situation I |

Situation II |

| Net Total Income |

5,00,000 |

5,00,100 |

| Computation of Tax |

|

|

| 0-250000 @0% |

0 |

0 |

| 250001-500000 @5% |

12500 |

12500 |

| 500001-500100 @20% |

0 |

20 |

| Rebate u/s 87A |

12500 |

0 |

| Net Tax |

0 |

12520 |

| Add: Cess @ 4% |

0 |

501 |

| Net Tax Liability |

0 |

13201 |

Note: An individual having a Gross Total Income of Rs 6,50,000 with eligible investments and deductions under Chapter VI A will be able to enjoy a tax-free Income as his Net Taxable Income will be Rs 5,00,000 which is eligible for full rebate under Sec 87A.

- Increase in standard deduction from INR 40,000 to INR 50,000 for Salaried employees

- Prescribed monetary threshold for deduction of tax on interest from bank or Post Office deposits increased from INR 10,000 to INR 40,000

Income from House Property

- Relief for owners of more than one house; second self-occupied house not to be subject to tax on deeming/notional basis; aggregate deduction of interest on home loan for self-occupied properties retained at INR 2,00,000

Capital Gains

- Proportionate exemption on long-term capital gains arising from proceeds of sale of residential house extended to purchase of two residential houses from one house, subject to Amount of capital gain not exceeding INR 2 crore [no monetary threshold continues for investment in one residential house] and it is a One-time opportunity to claim such exemption

Benefits to Construction Sector:

In the Affordable Housing sector, benefits under Section 80-IBA of the IT Act were extended by a year for projects approved till March 2020. This will allow Real Estate developers to deduct 100% of profits derived from development of affordable housing projects. Extension of benefits in the real estate sector will give a boost to construction activity, particularly in affordable housing.

Exemption from levy of notional rent on unsold inventories from one year to two years is an additional boon to the real estate industry which is bogged down with huge unsold inventories. The period would be counted from end of the year in which projects get completed.

From the consumers’ point of view, benefits of rollover in capital gains and exemptions on income tax on rent will boost housing demand, and is also expected to increase investments in a second house.

In the previous issue published in Jan 2019, we understood how the residential status of an Individual is determined under FEMA. Having known that, let’s travel further to understand how does a Non-Resident manage his earnings in India with the bankers. It’s important to have a quick understanding of the definitions of an NRI as per FEMA.

Who is an NRI?

Non-Resident Indian (NRI) is defined in Regulation 2 of FEMA Notification No 5 dated May 3, 2000 as:

A person Resident outside India who is a citizen of India or is a Person of Indian Origin (PIO).

PIO is defined as:

A citizen of any country other than Bangladesh or Pakistan, if

- he at any time held Indian Passport, or

- he or either of his parents or any of his grand-parents was a Citizen of India by virtue of the Constitution of India or the Citizenship Act, 1955 (57 of 1955) or

- the person is a spouse of an Indian Citizen or a person referred to in sub clause (a) or (b)

NRO (Non-Resident Ordinary Account)

Now, let’s get some basic questions on NRO Account answered:

| Questions |

Answers |

| Who can open an NRO Account? |

Any Person resident outside India |

| Why is an NRO account opened? |

To put through bona fide transactions in Rupees not involving any violation of FEMA Act, rules and regulations. |

| Prohibitions from NRO |

The operations in the accounts should not result in the account holder making available foreign exchange to any person resident in India against reimbursement in rupees or in any other manner. |

| When is RBI Approval needed for NRO Account opening? |

Opening of accounts by entities of Bangladesh Ownership and by individuals/entities of Pakistan nationality /ownership. |

| Can a Non-Resident open an maintain an account with Post Office? |

Yes, same terms and conditions as applicable to NRO accounts with Banks to be followed. |

| Types of Accounts that can be maintained as NRO |

Current, Savings, Recurring Deposits, Fixed Deposits. |

| Joint Holding Possible? |

Yes, a Non-Resident may hold an NRO account jointly with residents and or non-residents. |

PERMISSIBLE CREDITS/DEBITS INTO NRO ACCOUNT

Having understood what is an NRO account, who can open and operate it, let us move on to understand what are the permissible transactions for operations in an NRO Account.

| PERMISSIBLE CREDITS |

PERMISSIBLE DEBITS |

- Remittances from outside India through normal banking channels in Freely Convertible Foreign Currency.

- Freely convertible Foreign Currency physically deposited by the account holder during his temporary visit to India. If such amount exceeds USD 5000 or its equivalent, Currency Declaration Form to be submitted. Rupee funds to be substantiated by Encashment Certificate.

- Transfers from Rupee Accounts of Non-Resident Banks.

- Income in India like Rent, Dividends, Pension, Interest, Sale proceeds of Immovable Property in India (acquired or inherited) etc.,

- Rupee gift received from a Resident Individual who is a close relative by way of crossed cheque/ electronic transfer. The gift amount cannot exceed USD 1,25,000 per year as per the Liberalized Remittance Scheme available to Resident Individuals.

- Loan received from a Resident Individual who is a close relative by way of crossed cheque/ electronic transfer. The Loan amount cannot exceed USD 1,25,000 per year as per the Liberalized Remittance Scheme available to Resident Individuals.

|

- All local payments in Rupees including payment for Investments in India subject to compliance of FEMA regulations as applicable.

- Remittance outside India of current Income like rent, dividend, pension, interest etc. in India of the account holder after payment of due taxes in India.

- Remittance up to USD 1 million per financial year (April- March), for all bona fide purposes.

- Transfer to NRE Account of the NRI within the overall limit of USD 1 million in a financial year subject to payment of tax as applicable.

|

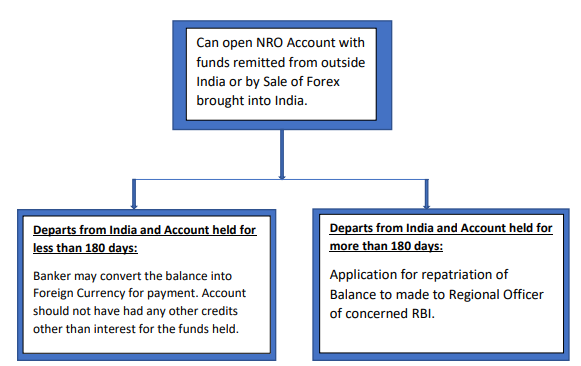

SPECIFIC PROVISIONS RELATING TO REMITTANCE OF ASSETS

There will be situations where a Foreign national who was Resident in India for employment reasons will leave India on account of his retirement. There will also be situations for a PIO or NRI to Inherit assets in India. In this section, we will understand the limits available for remittance of such assets and the conditions attached to it.

Restrictions in Remittances:

In respect of Immovable Property: Not available to citizens of Pakistan, Bangladesh, Sri Lanka, China, Afghanistan, Iran, Nepal and Bhutan. Prior Permission of RBI is required.

In respect of other financial assets: Not available to citizens of Pakistan, Bangladesh, Nepal and Bhutan.

FOREIGN NATIONALS OF NON-INDIAN ORIGIN ON VISIT TO INDIA:

When should a normal account be changed to NRO and vice versa?

a) From Resident to Non-Resident:

- When person resident in India leaves India (other than Nepal or Bhutan) for employment or business or vocation or for any other purpose indicating his intention to stay outside India for an uncertain period.

b) From Non-Resident to Resident:

- On the return of account holder to India for taking up employment, or for carrying business or vocation or for any other purpose indicating his intention to stay outside India for an uncertain period. (Temporary visits aren’t covered).

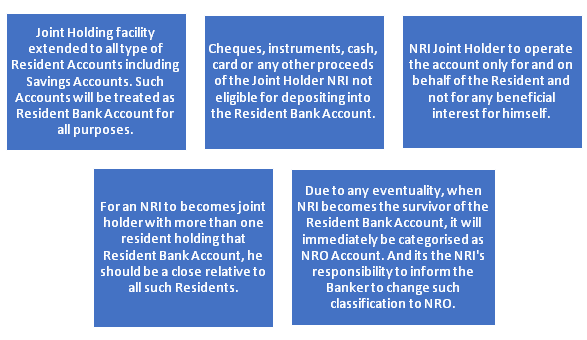

Resident Bank account maintained by residents in India- Joint Holder- Liberalization

We all are aware of the extant of emigration that is happening from India, where Indians leave to other country for career opportunities and find their livelihood there. We also witness the presence of elderly parents of many NRI’s living in India. The Government understanding the need and dependency of these elderly people with respect to operation of bank accounts by their children residing abroad, has brought in certain liberalization measures to permit resident Indians to include Non-Resident close relatives as Joint Holders on “Either or Survivor” basis. Let’s get an understanding of the rules and regulations prescribed in connection with such an account:

FOREIGN NATIONAL RESIDENT IN INDIA- ACCOUNT MAINTENANCE:

The Foreign Nationals employed in India holding valid visas are eligible to maintain resident bank accounts. When they leave the country, the accounts have to be closed and amounts have to be repatriated abroad. There might be situations that the Foreign Nationals have to hold the account for some more time to receive their legitimate dues in India. In such a scenario, the account has to be reclassified as NRO account by the Banker till such collection. The Banker would get an undertaking for the list of legitimate dues expected by the Foreign National and ensure only such dues get credited to the Bank Account.

The Repatriation limit will be the same USD 1 million per financial year subject to payment of all taxes as applicable in India and the account should be closed once all the money has been repatriated.

OPERATION OF NRO ACCOUNT BY POWER OF ATTORNEY HOLDER:

There are situations where a Non-Resident Individual would like operate his NRO account through a resident in India. Bankers can allow an NRO account to be operated by Power of Attorney Holder who is a resident in India, but is restricted to:

- a) All local payments including payments for eligible investments should be in compliance with the relevant regulations made by RBI.

- b) remittance outside India of current income in India of the non-resident account holder net of applicable taxes.

- c) The resident power of attorney holder is not permitted:

- to repatriate outside India funds in the account to anyone other than the non-resident account holder

- nor to make payment by way of gift to any resident on behalf of non-resident or

- transfer funds to another NRO account.

CONCLUSION

It’s very important for every individual who is not a resident in India to understand the intricacies of opening and operating an NRO account and also the benefits available to carry out smooth banking operations and manage the funds in India effectively.

PRIVATE PLACEMENT OF SHARES BY A PRIVATE COMPANY

Every Business Expansion demands lot of financial investment by the promoters. The Promoters many a time find it essential to source such additional funding from their close relatives or friends. There are also groups of Venture Capitalists, Angel Investors who invest in promising ideas and technology that a Startup works on. We witness an increase in the number of youngsters who choose to be entrepreneurs with innovative ideas. Since Private Limited Companies by definition and nature are not allowed to go public to meet their funding requirements, a special provision for raising funds from a selected group of persons is made available by Companies Act 2013, the terms and conditions of which is prescribed under Section 42. Such special provisions made available to a Private Limited Company is termed as Private Placement.

This Article focuses on giving the reader an understanding the process involved in raising funds through Private Placement Route.

First, let us understand the definition of Private Placement under the Companies Act 2013:

As per Section 42, of Companies Act 2013(as substituted by the Companies Amendment Act 2017 effective from 7th August 2018) (, “Private placement” means any offer or invitation to subscribe securities to a selected group of persons (referred to as “identified persons” whose number shall not exceed fifty or such other higher number *as may be prescribed, excluding (**Qualified Institutional buyers and employees covered by ESOP Scheme) by a company through issue of Private Placement Offer Letter in a financial year subject to such conditions as may be prescribed.

A company cannot make a public announcement for such Private Placement offers.

*the number of persons to whom offer or invitation to subscribe is prescribed as 200, so a company cannot exceed this number in a financial year (applies to each kind of security offered).

*“Qualified institutional buyer’’ means the qualified institutional buyer as defined in the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009 as amended from time to time under the Securities and Exchange Board of India Act 1992.

Conditions:

- Every identified person willing to subscribe to the private placement issue shall apply in the private placement and application issued to such person along with subscription money paid either by cheque or demand draft or other banking channel and not by cash.

- The Company shall not utilize the funds raised through private placement unless allotment is made and the return of allotment is filed with the Registrar of Companies.

- No fresh offer or invitation under this section shall be made unless the allotments with respect to any offer or invitation made earlier have been completed or that offer or invitation has been withdrawn or abandoned by the company.

- Allotment to be completed within 60 days of receipt of money, if unable to do so, the Company should refund the application money within 15 days from the expiry of 60 days. In the event of failure of the Company to pay back the application money with 15 days, interest to be paid at 12% per annum from the expiry of sixtieth day.

Procedure for Issue of Securities through Private Placement

Step 1: Board Meeting for Matter in relation to Pre-activity of PP

- The first step in Issue of Shares through Private Placement is to verify the Articles of Association of the company to give effect to Private Placement. If the AOA does not provide the same, then the company shall alter the AOA. Then the Company shall decide upon the Identified Persons to whom the Private Placement is to be issued.

- The Company shall conduct Board Meeting and pass resolution to meet the following agendas i.e. to alter the Articles of Association, to increase the Authorized Capital if required and to consider and approve the Letter of the Offer and issue a Notice calling for a General Meeting.

- The Company shall open a Separate Bank Account in a Scheduled bank for depositing the Application Money to be received.

- The Board shall finalize the list of the Investors for issuance of new Equity Shares.

DISCLOSURES IN EXPLANATORY STATEMENT ANNEXED TO NOTICE FOR SHAREHOLDER’s APPROVAL:

Particulars of the offer including date of passing of Board Resolution

Kinds of securities offered and the price at which security is being offered

Basis or justification for the price (including premium if any)

Name and address of the valuer who performed valuation

Amount which the company intends to raise by way of such securities

Material terms of raising such securities, proposed time schedule, purposes or objects of offer, contribution made by promoters or directors either as part of offer or separately in furtherance of objects, principal terms of assets charged as securities.

Step 2: Conduct of Extra-Ordinary General Meeting (EGM)

In the Second Step, the Shareholders have to approve the issue by way of Private Placement by way of a special resolution for each of the offers or invitations at the General Meeting called for by the Board for this purpose.

- Offer cum application letter shall be in the Form prescribed PAS – 4 serially numbered and addressed to the person to whom offer is made.

- The Form PAS – 4 & PAS – 5 is to be circulated in the General Meeting.

- Form PAS – 4 shall include the Details of the Offer, Financial Position of the Company, any disclosures of interest of the Directors and Declaration by the Directors.

- Form PAS – 5 shall include the personal details of the persons to whom the Offer Letter is to be circulated.

- A Special Resolution is to be passed in the Extraordinary General Meeting to alter the Articles of Association and for Issuance of Equity Shares on Private Placement Basis.

- An Ordinary Resolution is to be passed for Increase in Authorized Share Capital, if any.

Note: Form PAS – 4 and Form PAS – 5 need not be filed with the Registrar by the company, and is enough if maintained by the Company in its records.

Step 3: Issuance of Offer Letter

The Offer Letter being approved in the General Meeting is to be sent to the Identified Persons to whom the Private Placement is to be done either through post or electronic mode or in person.

Prior to issuing the Offer Letter, the special resolution approving the issuance of securities and/or board resolution for issue of securities has to be filed with the ROC. In this regard, it has also been clarified that private companies (which were earlier exempted from filing of board resolutions) will have to file board resolutions passed for issue of securities.

Step 4: Receipt of Application Money

Application Money received shall be deposited in the Separate Bank Account in a Scheduled Bank. The Share Application Money is to be received only through cheque or demand draft or any other banking channel other than Cash.

The Share Application Money received are not to utilized for any other purpose other than

- For adjustment of allotment of securities; or

- For the repayment of monies by the company to those who subscribed, when unable to allot securities.

Step 5: Board Meeting for Allotment of Securities

The final step in Private Placement of shares of Private Company is the allotment of securities by passing a Board Resolution in a Board Meeting. After allotment, the company is to file an e-form PAS – 3 with the Registrar including the following details:

- Personal Details

- Class of security allotted

- Number of securities held, nominal value and particulars of consideration

- Date of allotment of security

Time Limit for Allotment

Allotment of Securities is to be completed within 60 days from the date of receipt of Share Application Money. On default of allotment, the company shall repay the Application Money within 15 days. On default of repayment, interest of 12% is to be paid from the expiry of sixtieth day.

A return of allotment to be filed within fifteen days from the date of the allotment in such manner as may be prescribed, including a complete list of all allottees, with their full names, addresses, number of securities allotted and such other relevant information as may be prescribed.

PENALTIES

If a company defaults in filing the return of allotment within the period prescribed under sub-section (8), the company, its promoters and directors shall be liable to a penalty for each default of one thousand rupees for each day during which such default continues but not exceeding twenty-five lakh rupees.

Subject to sub-section (11), if a company makes an offer or accepts monies in contravention of this section, the company, its promoters and directors shall be liable for a penalty which may extend to the amount raised through the private placement or two crore rupees, whichever is lower, and the company shall also refund all monies with interest as specified in sub-section (6) to subscribers within a period of thirty days of the order imposing the penalty.

Sample Resolution Formats

Clause for Alteration of AOA:

“Further issue of shares may be made in any manner whatsoever as the Board may determine including by way of preferential offer or private placement, subject to and in accordance with the Act, Rules and other applicable provisions of law.”

Clause for Approval of allotment of equity shares:

“RESOVED THAT pursuant to the provisions of Section 42 of the Companies Act 2013 read with Rule 14 of Companies (Prospectus and Allotment of Securities) Rules, 2014 and such other provisions (including any statutory modifications or re-enactment thereof) as may be applicable for the time being in force, and subject to the approval of members in general meeting, consent of the board of directors of the Company be and is hereby accorded for offering, issuing and allotting ______- no of equity shares (in words) at a face value of Rs ___ each and that draft letter of offer in Form PAS-4 for issue of such securities and record for Private Placement in PAS-5,a s placed before board, be and are hereby approved.

“RESOLVED further that” Mr./Ms. __________of the Company be and is hereby authorized to sign and circulate the letter of offer in Form PAS-4 along with the application form to _________ (Name of Offeree/ said offerees), whose names is/are recorded in Form PAS-5 i.e. Record of Private Placement Offer

RESOLVED further that” Mr./Ms. __________of the Company be and is hereby authorized to file the necessary forms with the Registrar of Companies and to make necessary entries in the applicable registers including but not restricted to the Register of Members for the aforesaid issue and allotment of equity shares.